In November 2025, the UK government has revised its proposed international student levy, marking a notable shift in how additional funding contributions from the sector will be calculated. The policy, first outlined as part of a broader effort to stabilise higher education finances and reduce reliance on international fee income, initially proposed a 6 per cent tax on total international tuition revenue. This approach drew significant attention across the sector, with many institutions warning it would disproportionately impact providers with large international cohorts and tighter operating margins.

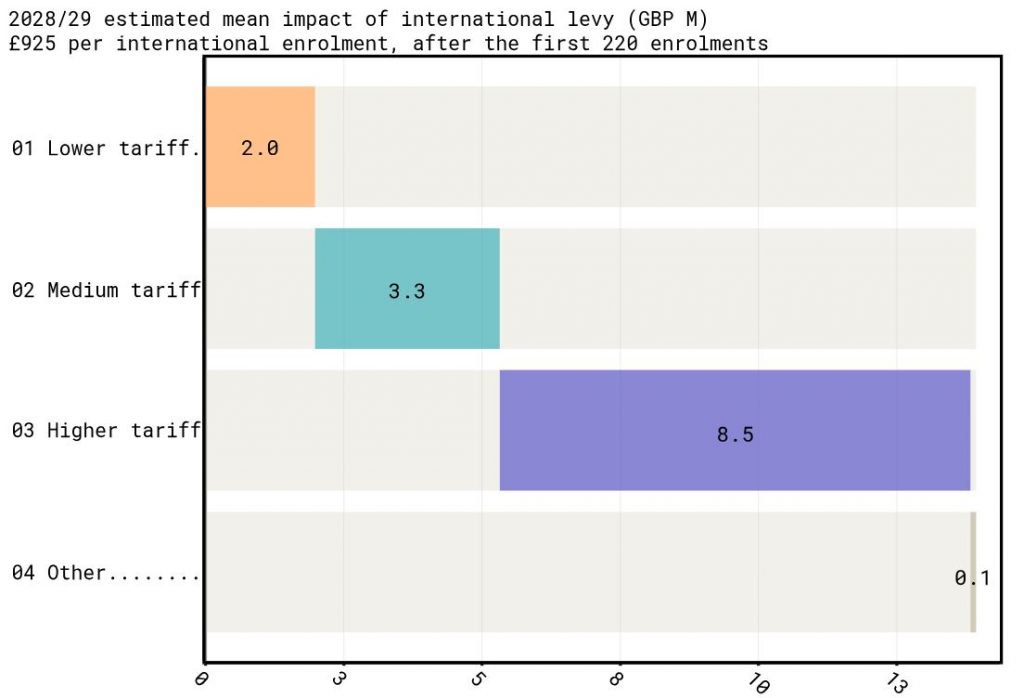

Following consultation and sector feedback, the government has now replaced the percentage-based model with a fixed per-student charge. Under the revised proposal, providers will pay £925 for each international enrolment, with the first 220 students exempt from the levy. This adjustment introduces a more tapered cost structure, reducing the marginal impact on institutions with smaller international populations while capping exposure for larger, higher-tariff providers.

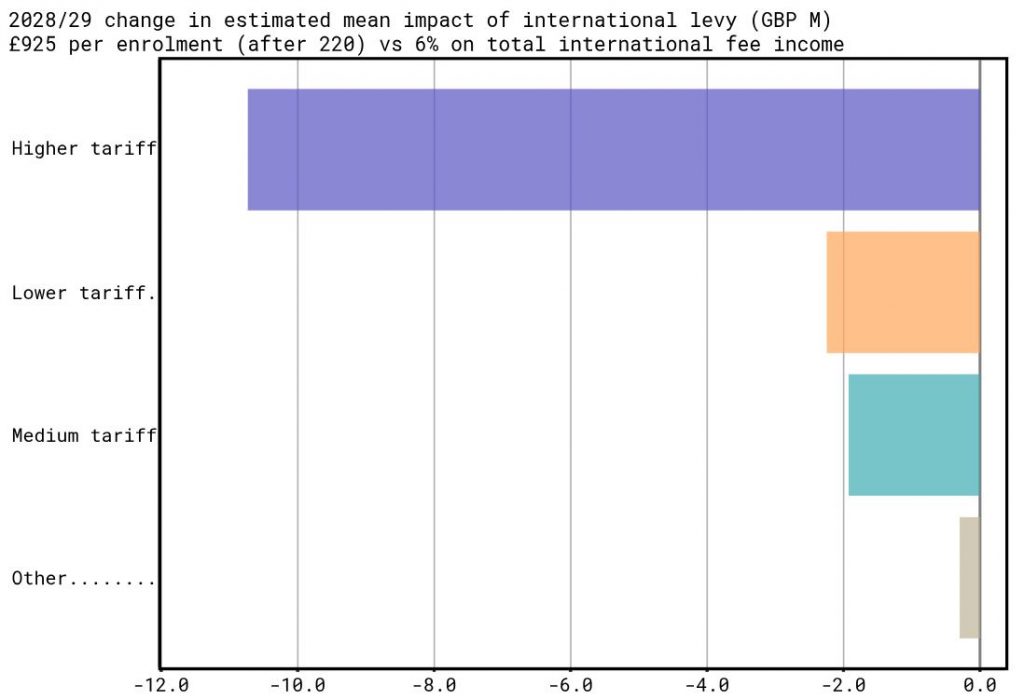

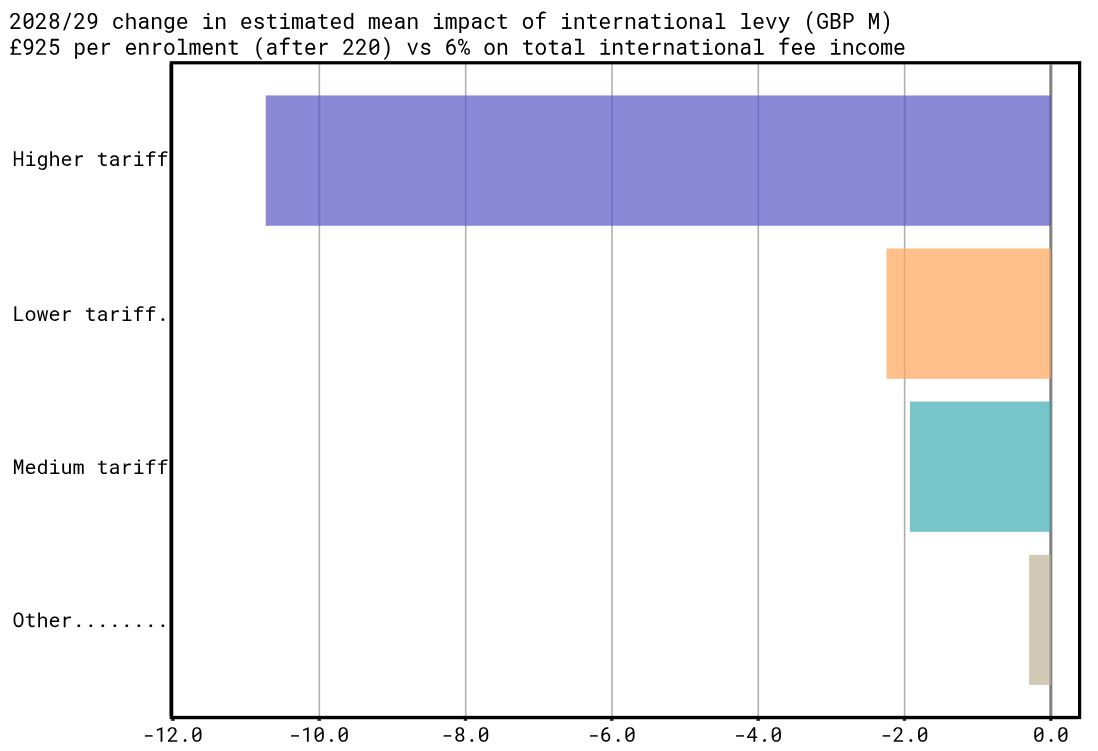

The change materially alters the distributional effects of the levy. Under the original 6 per cent model, costs scaled directly with fee income, placing the greatest burden on institutions with both high volumes of international students and premium fee levels. By contrast, the new flat-rate approach weakens the link between fee price and levy contribution, shifting relative advantage towards higher-tariff institutions that typically command higher fees per student.

Modelling suggests that, on average, these institutions stand to benefit significantly from the revision, with projected savings exceeding £10 million annually by 2028/29 compared to the original design. Meanwhile, providers with lower fee levels and more price-sensitive recruitment profiles may see comparatively smaller gains, or in some cases a higher effective levy per pound of fee income.

The charts below illustrate how the revised structure reshapes the sector-wide distribution of costs (Figure 1), as well as the scale of savings across different provider groups (Figure 2). Together, they highlight a policy pivot that retains the government’s objective of extracting additional resource from international recruitment, but does so in a way that redistributes financial pressure and moderates the impact on the sector’s highest-earning institutions.